A government announcement has set tuition fees in England on a rising path once more

In October, the UK Government announced a range of changes for post-16 education. What grabbed headlines were details of the proposed new ‘V Levels’, which will be “new vocational qualifications tied to rigorous and real-world job standard”. V Levels will form part of a new educational goal for two-thirds of young people to participate in higher-level learning – academic, technical, or apprenticeships – by age 25.

The Department of Education (DfE) press release included further news, which gained less coverage:

- University tuition fees in England will rise in line with forecast (unspecified) inflation for the next two academic years.

- Thereafter, subject to the introduction of new legislation, future years will see automatic increases in line with inflation.

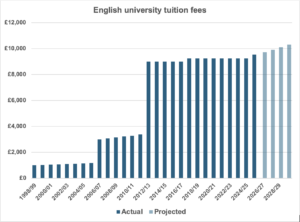

As the graph above shows, even if the assumed and actual inflation is 2%, then by the 2028/29 academic year, English tuition fees will have crossed the £10,000 threshold – ten times their 1998/99 starting level.

Tuition fees are a different matter in other parts of the UK – in Scotland, for example, there are no fees for Scottish students attending Scottish universities. However, what England decides on fees plays a major role, both in terms of setting the tone and the level of tuition fees paid by students in Scotland, Wales and Northern Ireland, if they choose a university outside their home country.

The announcement of the new tuition fee escalator comes two years after a major change to the way student loans operate for new undergraduates in England; those who started their course before 2023/24 were unaffected. The latest loan rules – known as Plan 5 – have three important features:

- Repayment is at the rate of 9% of income over £25,000 (frozen until at least 2027), starting in the April after leaving university.

- Interest is charged at the rate of the Retail Price Index (RPI) inflation in March of each year (3.2% for 2025).

- Any loan outstanding at the end of 40 years (or on death) is automatically written off.

Those terms apply to all student loans – both maintenance and tuition fees – so could cover £60,000 of debt for a new graduate. However, before you consider paying up front for your child’s (or grandchild’s) higher education, do take financial advice, as it may not be the most sensible option.

The value of your investment and any income from it can go down as well as up and you may not get back the full amount you invested. All statements concerning the tax treatment of products and their benefits are based on our understanding of current tax law, financial planning strategies and HM Revenue and Customs practice. Levels and bases of tax relief are subject to change and vary according to individual circumstances. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances. Past performance does not guarantee future performance. Every effort has been made to ensure the information in this post is accurate at the time of publication. The Financial Conduct Authority does not regulate tax or will advice.